Managed Inference Cost Analysis: Where API Pricing Stops Working for Agent Workloads

A single infrastructure strategy does not hold across workload types. At standard API volume, per-token pricing is the cost leader. At agent scale, fixed-cost infrastructure takes over.

What We Analyzed

This analysis evaluates 11 provider/model combinations using published list prices as of February 21, 2026 across two operating regimes:

- Standard API workload: 100M tokens/month

- Agent workload: 1.6B tokens/month

Every provider is scored with one canonical cost model:

monthly_cost = (input_tokens/1M × input_rate) + (output_tokens/1M × output_rate) + fixed_monthly + egress

We also apply overhead assumptions (retry, guardrails, caching) and quality/SLA filters before ranking providers.

Recommendation up front:

- For predictable API workloads under ~1B tokens/month, stay with pay-per-token providers.

- For sustained agent workloads around or above ~1B tokens/month, evaluate fixed-cost infrastructure immediately.

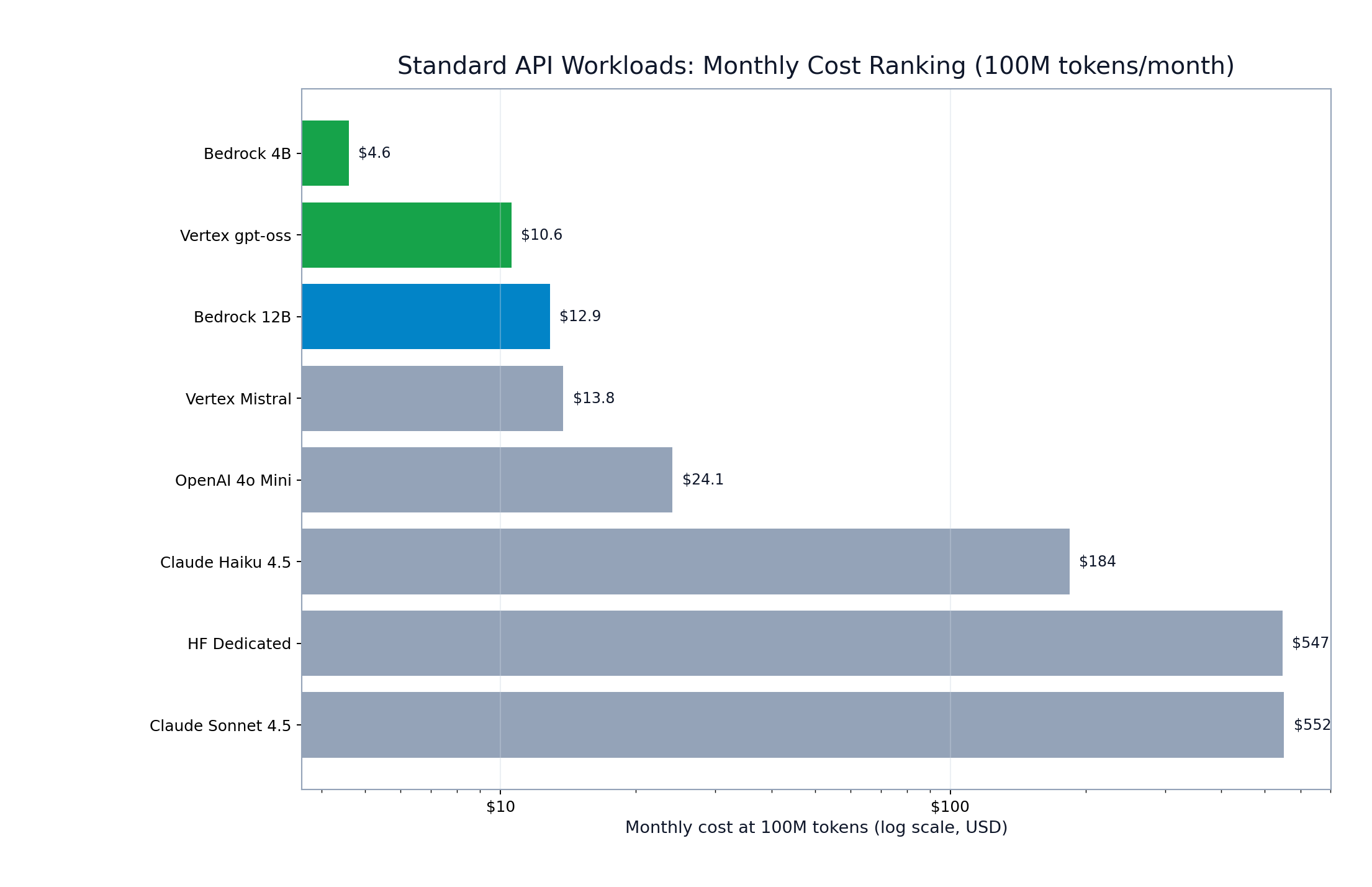

Key Findings at 100M Tokens/Month

At standard API volume, pay-per-token providers dominate on cost. The cheapest tier-4 options stay in the low double-digits per month.

Standard API ranking (directional)

| Rank | Provider | Monthly Cost (100M) |

|---|---|---|

| #1 | Bedrock Gemma 3 4B | ~$4.6 |

| #2 | Vertex gpt-oss | ~$10.6 |

| #3 | Bedrock 12B | ~$12.9 |

| #4 | Vertex Mistral | ~$13.8 |

The practical default for quality/cost balance is Bedrock 12B (~$12.9/mo) when tier-4 quality is required.

Standard API monthly ranking at 100M tokens

Standard API monthly ranking at 100M tokens

FIGURE 1: Standard API ranking at 100M tokens/month (log-scale x-axis to show spread across providers).

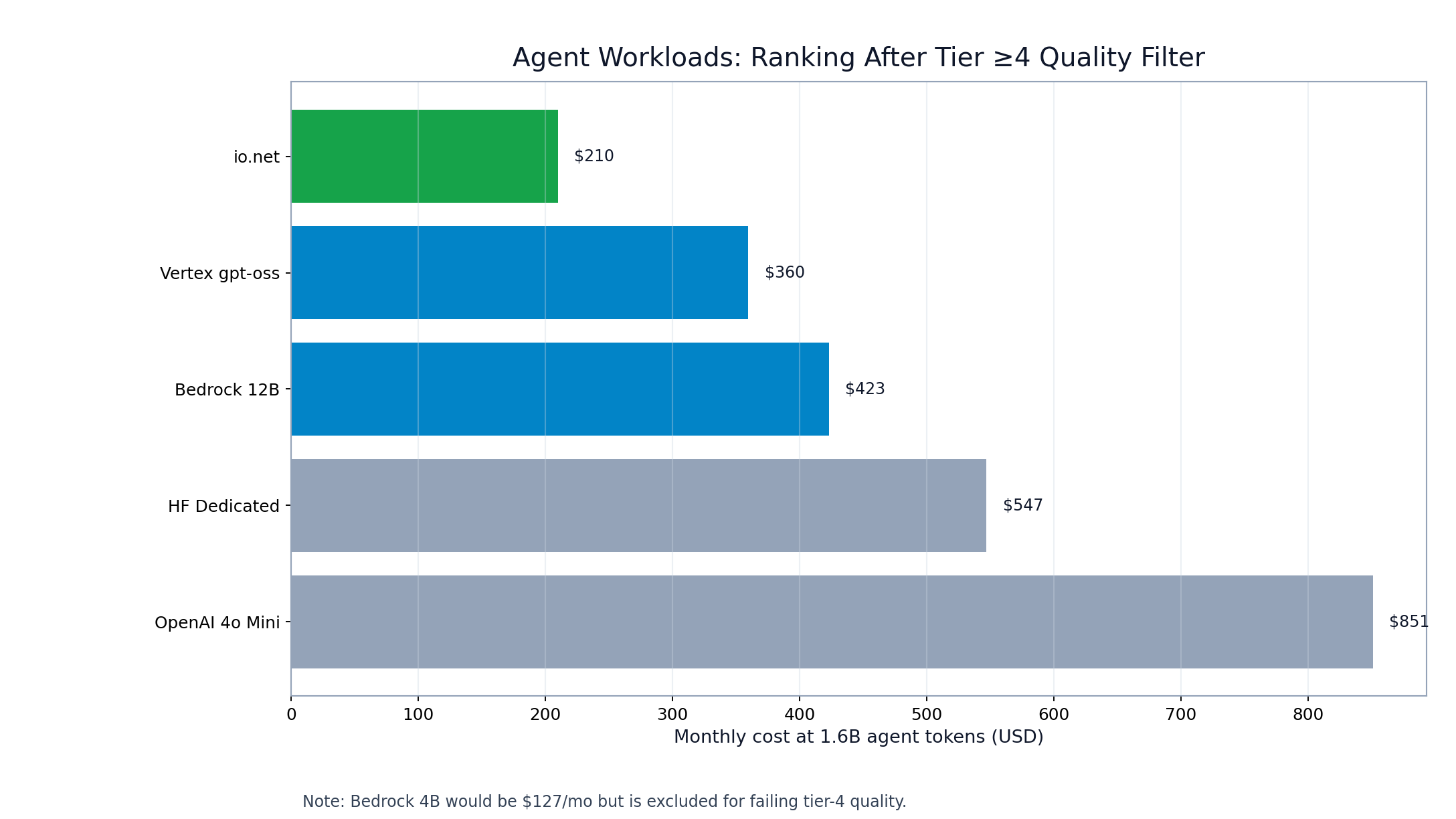

Why Agent Workloads Flip the Ranking

Agent assumptions materially change the economics:

- Input/output mix shifts to 35/65 (output-heavy)

- Net overhead increases to ~1.20x

- Minimum quality threshold increases to tier >= 4

Under that profile, costs that looked negligible in API mode scale sharply for per-token pricing, while fixed-cost options remain flat.

Agent ranking at 1.6B tokens/month (tier >= 4)

| Rank | Provider | Monthly Cost (Agent) |

|---|---|---|

| #1 | io.net | ~$210 |

| #2 | Vertex gpt-oss | ~$360 |

| #3 | Bedrock 12B | ~$423 |

| #4 | HF Dedicated | ~$547 |

| #5 | OpenAI 4o Mini | ~$851 |

Agent workload monthly ranking at 1.6B tokens

Agent workload monthly ranking at 1.6B tokens

FIGURE 2: Agent ranking after applying tier >= 4 quality filter. io.net leads at 1.6B tokens/month.

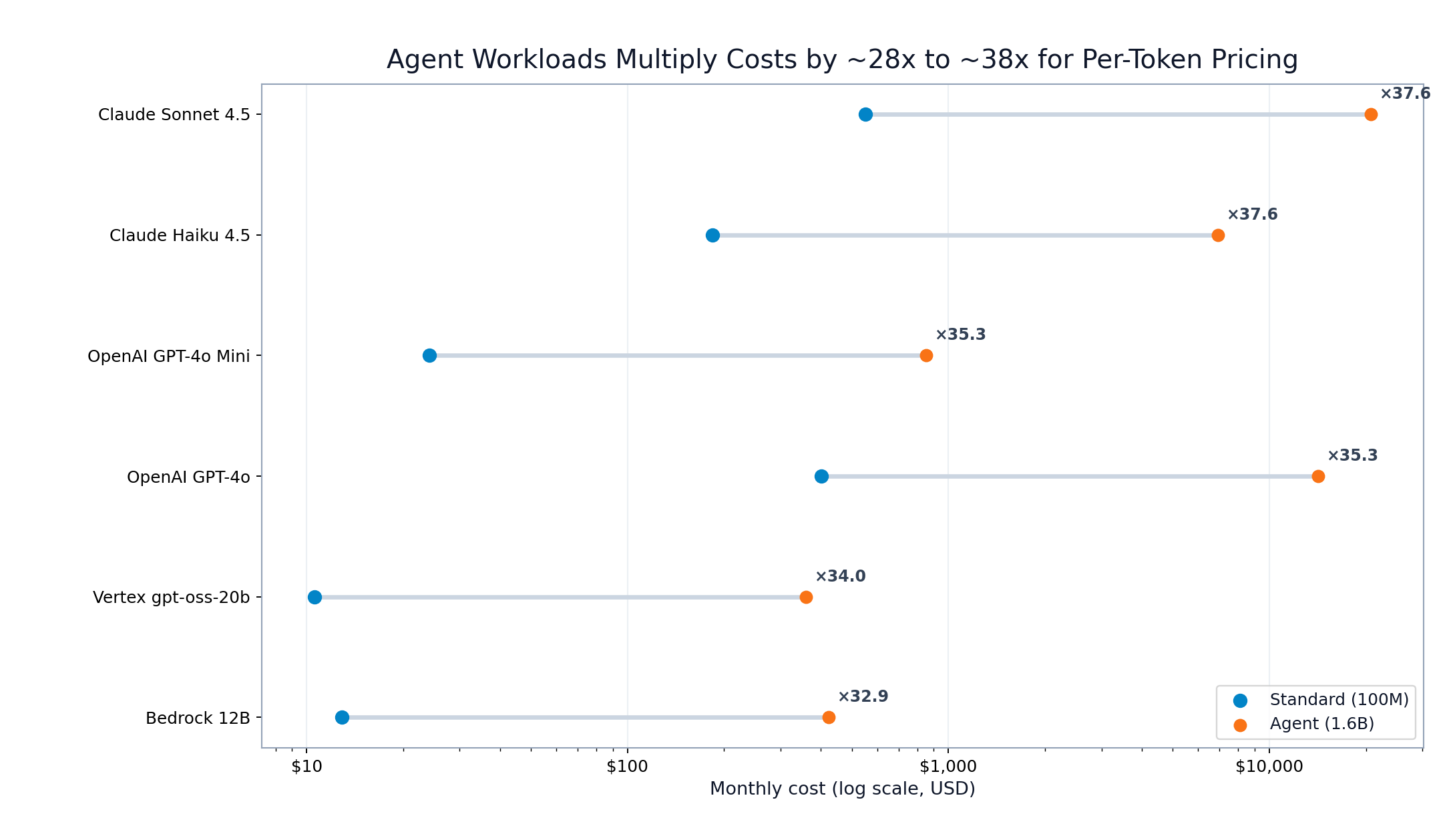

The magnitude of change is the operational shock. Per-token providers rise by roughly 28x to 38x from standard mode to agent mode.

Agent-to-standard monthly cost multipliers by provider

Agent-to-standard monthly cost multipliers by provider

FIGURE 3: Agent workloads multiply per-token costs by ~28x to ~38x across major providers.

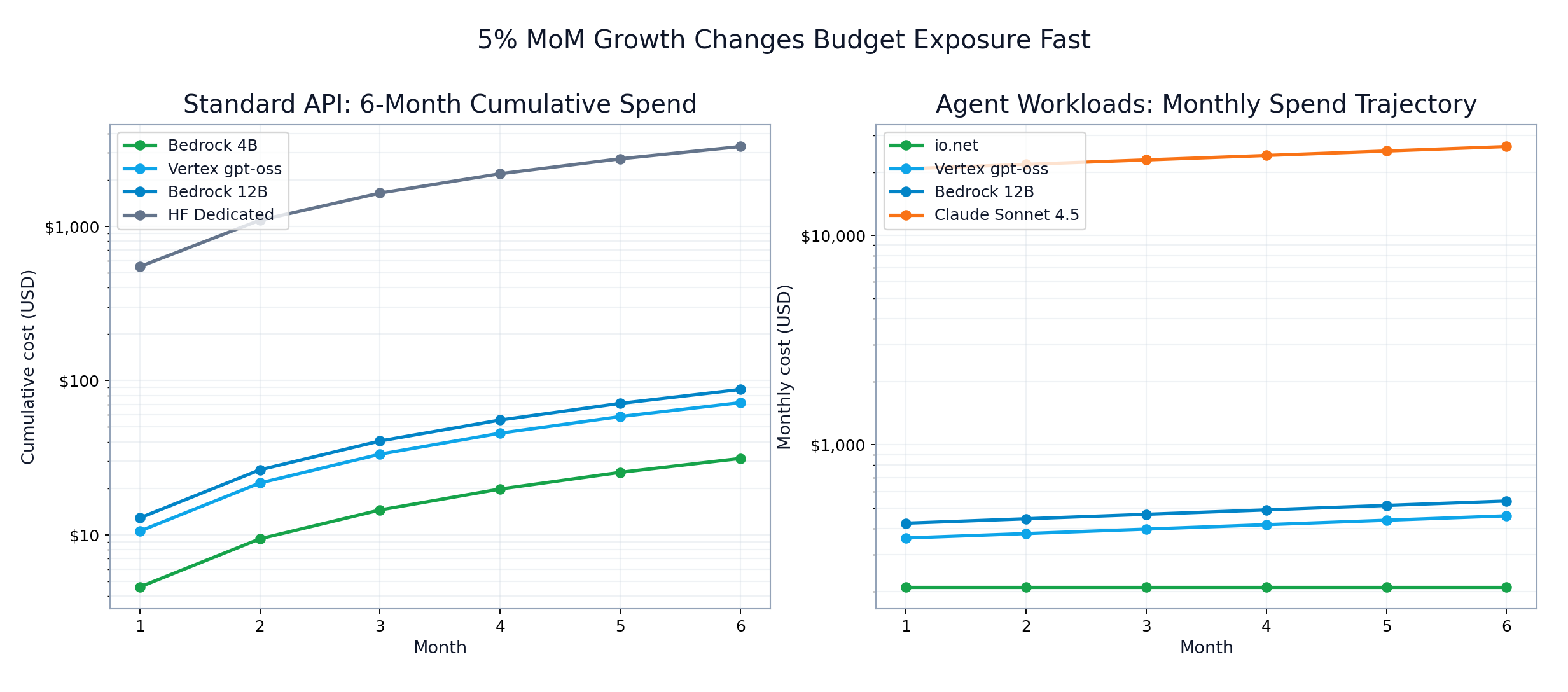

The 6-Month Budget Reality

With 5% month-over-month volume growth, short-term budget exposure diverges quickly:

- io.net: ~$1.26K over 6 months (flat monthly profile)

- Vertex gpt-oss: ~$2.45K over 6 months

- Bedrock 12B: ~$2.88K over 6 months

- Claude Sonnet 4.5: ~$141K over 6 months

This is why agent infrastructure choices are not just optimization decisions; they are budget-shaping decisions.

Six-month standard and agent cost forecast

Six-month standard and agent cost forecast

FIGURE 4: Two-panel 6-month view: standard cumulative spend (left) and agent monthly trajectory (right).

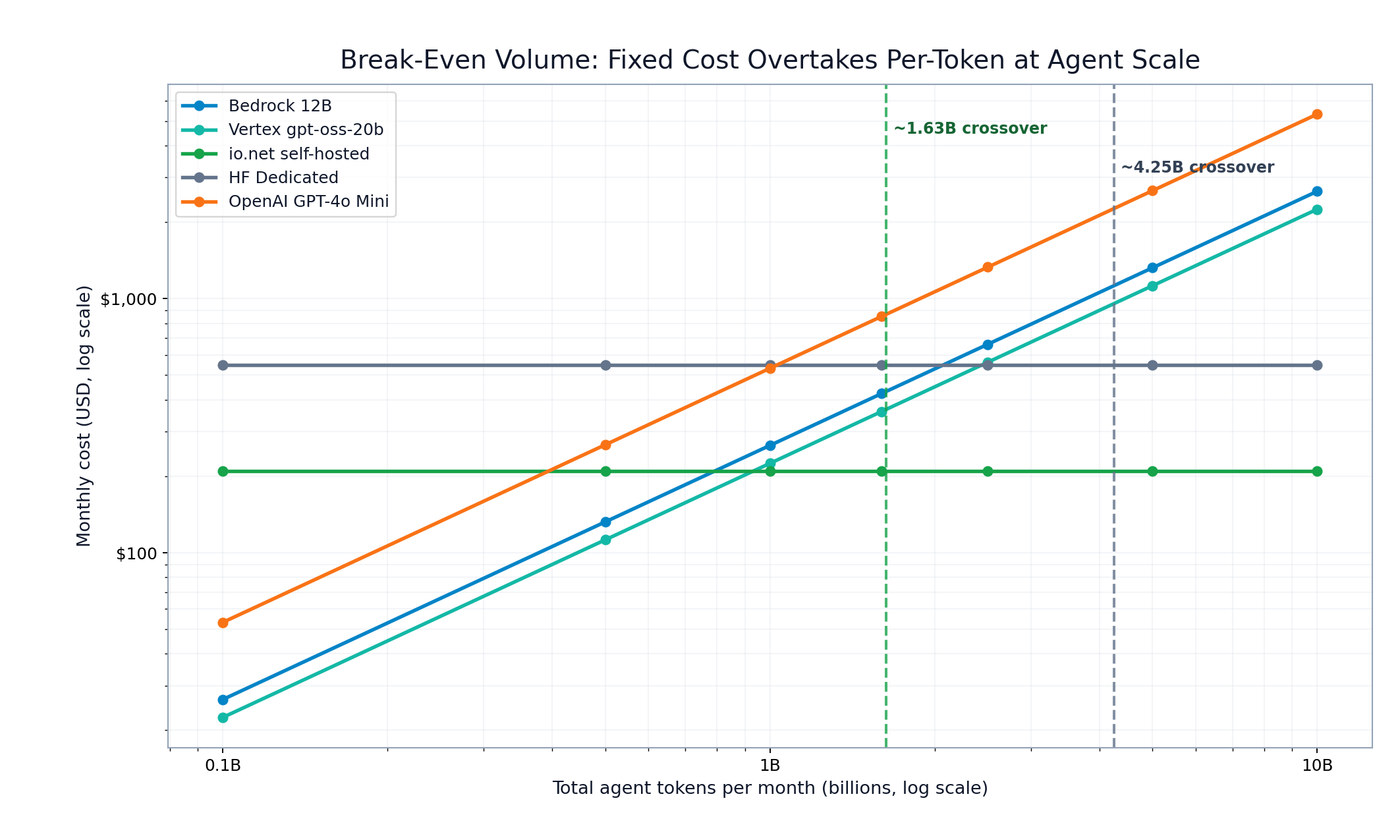

Break-Even Thresholds That Change Decisions

The key thresholds are explicit:

- io.net vs Bedrock 12B: break-even at ~1.63B tokens/month

- HF Dedicated vs Bedrock 12B: break-even at ~4.25B tokens/month

Interpretation:

- Below ~1B agent tokens/month, pay-per-token can still win.

- Around and above ~1B to ~1.6B sustained tokens/month, fixed-cost options become structurally advantaged.

Break-even and crossover by monthly agent token volume

Break-even and crossover by monthly agent token volume

FIGURE 5: Volume crossover map (log-scale). Exact modeled break-even points: 1,631,720,649 and 4,250,243,787 tokens/month.

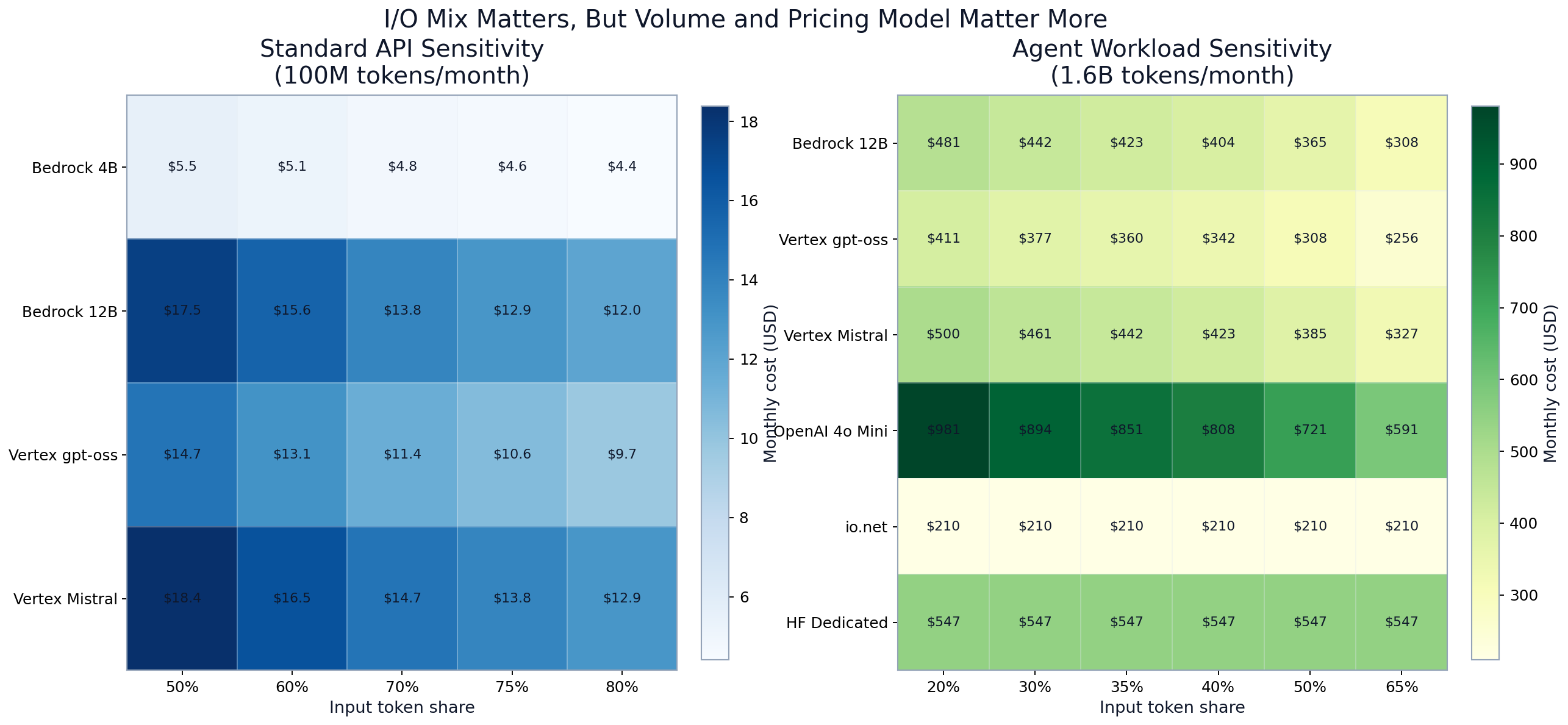

Sensitivity: What Matters Most

Two things can be true simultaneously:

- I/O ratio matters: output-heavy workloads materially increase per-token spend.

- Volume and pricing model matter more: fixed-cost options stay flat while per-token lines keep climbing.

In standard API mode, rankings remain stable across tested I/O mixes. In agent mode, I/O changes move costs, but they do not erase the fixed-cost advantage at sustained high volume.

Sensitivity heatmaps for standard and agent I/O ratio shifts

Sensitivity heatmaps for standard and agent I/O ratio shifts

FIGURE 6: Sensitivity heatmaps. Standard API remains low-cost under tested ratios; agent mode remains structurally cost-heavy for per-token pricing.

Decision Framework

Use this as an operating policy:

- If you are in standard API mode and below sustained billion-token volume, optimize within pay-per-token.

- If you are in agent mode and approaching sustained billion-token volume, run fixed-cost infra evaluation now.

- Enforce tier >= 4 quality for production agents before final cost comparisons.

Assumptions and Limitations

- Pricing uses published list prices as of February 21, 2026; enterprise discounts are excluded.

- Quality tier scores are estimated by model class and should be validated against your own eval suite.

- SLA/latency values for some providers are estimated and may differ by region and contract terms.

- io.net pricing is marketplace-dynamic; modeled fixed cost is a reference estimate, not a guaranteed quote.

- Agent assumptions (tasks, calls/task, tokens/call, overhead) are illustrative and should be replaced with your production telemetry.

- Model excludes some second-order costs (for example, advanced networking or multi-region replication add-ons).

Related Reading

- How We Built the Inference Cost Forecasting Model: Technical Methodology

- The Hidden Economics of Token-Based LLM Pricing: Why Your AI Costs Are Unpredictable

- Building Production Token Analytics: Technical Implementation Guide

- AI Observability Tools: Which One Actually Fits Your Problem?

Methodology baseline: published list-price snapshot dated February 21, 2026.

Want fewer escalations? See a live trace.

See Briefcase on your stack

Reduce escalations: Catch issues before they hit production with comprehensive observability

Auditability & replay: Complete trace capture for debugging and compliance